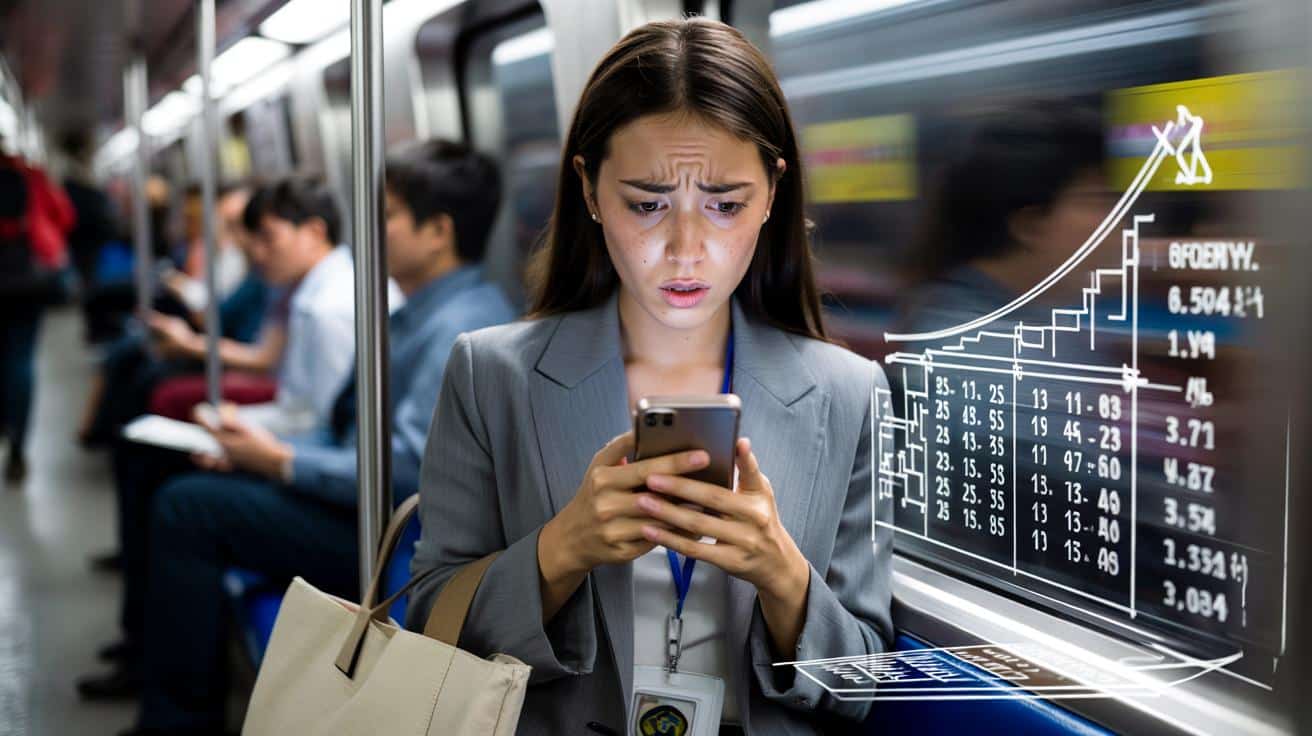

The email landed in her inbox at 7:42 a.m., just as her subway car jolted out of the tunnel. Lauren blinked at the subject line: “Important Notice About Your Student Loan Account.” She’d been so proud of herself. Automatic payments set. Never missed one. Coffee in one hand, phone in the other, she tapped open the message, expecting a boring confirmation.

Instead, she froze.

Her balance wasn’t going down. It was growing. And right there, in black and white, was the number that made her throat tighten: **17.02% interest rate**.

Lauren thought there had to be a glitch. She’d been doing everything “right.” Paying above the minimum, skipping dinners out, cancelling Netflix, saying no to a weekend trip with friends.

Now she was staring at a reality she didn’t even know was possible.

Someone was getting rich off her degree.

“I thought I was winning. I was barely treading water.”

When Lauren graduated from a mid-size state university, she didn’t feel naive. She’d sat through financial-aid briefings. She’d read the pamphlets. She’d even asked extra questions at the bursar’s office while her friends joked about never paying these loans back.

She signed her promissory notes online, clicked through disclosures, and told herself she’d handle it later. At 22, “later” feels far away. The numbers feel imaginary.

Three years into her first marketing job, “later” had arrived. Every month, $420 vanished from her checking account. She’d proudly screenshot her payment confirmations, the way someone might post gym selfies. It was proof she was responsible. Proof she was moving forward.

Except her total balance wasn’t really moving at all.

➡️ Sheets shouldn’t be changed monthly or every two weeks: an expert gives the exact frequency

➡️ He hid an AirTag in his sneakers before donating them: and traced them to a market stall

➡️ Neither boiled nor raw : the best way to cook broccoli to preserve maximum antioxidant vitamins

➡️ Neither tap water nor Vinegar: The right way to wash strawberries to remove pesticides

➡️ “I cleaned my home often but never felt it was fresh until this change”

➡️ Why this haircut is often misunderstood but works beautifully when done right

One rainy Tuesday, she finally opened the full loan statement instead of just scanning the payment line. That’s when she saw it. Out of her $420 payment, $320 went to interest. Only about $100 touched the principal.

The original $28,000 she’d borrowed for tuition and off-campus housing? After three years of “adulting,” her balance was… $27,600.

We’ve all been there, that moment when your stomach drops because the math doesn’t care how hard you’re trying.

Lauren called her servicer and spent 47 minutes listening to hold music and disclaimers. The representative, polite and rehearsed, walked her through the file. Mixed in with her federal loans was a private consolidation she didn’t fully remember agreeing to in her final semester. That one carried a variable rate that had quietly climbed to 17%.

The interest was eating every effort she made.

On paper, nothing illegal had happened to Lauren. She’d signed. She’d consented. She had clicked “I agree” like millions of other stressed-out 21-year-olds who just wanted to graduate.

But the structure of the debt was stacked against her from the start. High-interest loans don’t just slow progress. They reverse it. You can pay for years and still owe more than you started with.

That 17% rate meant her loan was acting less like an education investment and more like a credit card she never swiped. The compounding was relentless. Interest was calculated daily, added to the balance, and then the next day, interest was charged on top of that new, bigger number.

This is the quiet math behind so many “I thought I was paying it off” stories. People aren’t lazy or irresponsible. They’re stuck in contracts designed to pull them back every time they think they’re stepping forward.

How to stop your loan from quietly snowballing against you

The turning point for Lauren came when a co-worker casually said, “Send me a screenshot of your statement. All of it.” Not just the summary box, but the real breakdown: interest rate, capitalization, repayment term, every separate loan.

If you want a “first rescue move,” that’s it. Download the full statement, or log into your servicer and click on every single loan line. Write them down: lender, balance, interest rate, minimum payment.

Then circle anything in double digits. Anything over 10% is a red flag, and 17% is a siren. It doesn’t matter if it’s “only” one of your loans. That’s the one quietly burning holes in your future budget.

Seeing the numbers in one place is uncomfortable. *That discomfort is exactly what saves you from drifting another five years.*

Once Lauren knew which loan was killing her, she did something that felt almost too simple: she stopped spreading her extra money across all her loans. She attacked the 17% one first.

There’s a plain-truth sentence that every borrower should hear: **minimum payments are designed to serve the lender, not you**.

If you have multiple loans, paying a little extra on all of them sounds fair. It’s also one of the fastest ways to stay stuck. Channeling every spare dollar to the highest-interest loan while paying the minimum on the rest is what starts to flip the script.

She cut back where she could, picked up freelance design work, and funneled everything at that single monster loan. Watching that balance drop—even slowly—felt like getting oxygen back.

The mistake she regrets most isn’t taking out the loan. It’s waiting three years to really look at it.

During one of our calls, Lauren put it this way:

“I thought the hard part was graduating and getting a job. Nobody told me the real test would be paying for a degree on terms I didn’t fully understand.”

She’s not alone. Money coaches and legal aid counselors see this pattern every week. People pay faithfully, and the debt barely moves. So they blame themselves instead of the structure.

Here’s the short checklist that Lauren now sends to friends still in school or freshly graduated:

- Pull a full statement on every loan, not just the total.

- List balances and interest rates in order, highest rate first.

- Call your lender and ask directly about refinancing or fixed-rate options.

- Separate federal and private loans in your tracking sheet.

- Pick one “villain loan” and target it with every extra dollar you can.

She wishes someone had handed her that list at 19 instead of a glossy brochure with smiling graduates and tiny-font terms.

What Lauren’s story says about all of us

Lauren eventually refinanced that 17% loan down to single digits through a credit union she found almost by accident. The application wasn’t glamorous. No one rolled out a red carpet or congratulated her on beating the system.

But when the approval email came in, she cried in the break room. It wasn’t just about the lower rate. It was the first time she felt like she had any real leverage in a game she hadn’t realized she was playing.

Stories like hers sit in the background of the economy: quiet, spreadsheet-shaped, deeply human.

If you’re reading this and feeling that familiar knot in your stomach, you’re not alone—and you’re not behind. Many borrowers don’t fully grasp their rates, terms, or options until something jolts them awake. A scary email. A rejected mortgage application. A bank statement that just doesn’t add up.

The system relies on that fog. On people being too busy, too tired, or too intimidated to press pause and say, “Wait, what exactly am I paying for?”

There’s nothing noble about suffering in silence with a 15% or 17% loan you signed at 20. There is something quietly radical about pulling your own numbers, asking blunt questions, and refusing to accept that this is just how it has to be.

The next time you see a viral tweet about someone paying for a decade and still owing more than they borrowed, remember Lauren on that subway, staring at “17.02%.”

The fine print looks boring until it shapes your life.

Maybe tonight, before your next auto-debit goes out, you log in and read through the lines you once clicked past. Maybe you forward this story to the friend who jokes about dying with their loans.

Or maybe you’re the one who realizes that your “responsible” payment routine has been keeping someone else very comfortable. You don’t have to stay in that role.

| Key point | Detail | Value for the reader |

|---|---|---|

| Identify high-interest “villain” loans | Pull full statements, list each loan’s rate and balance, circle anything in double digits | Gives you a clear target instead of vague anxiety about “debt” |

| Prioritize payments strategically | Pay minimums on low-rate loans and send every extra dollar to the highest-rate one | Reduces total interest paid and speeds up real progress |

| Explore refinancing and fixed rates | Contact credit unions, reputable lenders, or nonprofit advisors to lower extreme rates | Lowers monthly pressure and stops interest from snowballing out of control |

FAQ:

- Question 1How do I find out my actual student loan interest rates?

- Answer 1Log into each loan servicer’s website and look at the detailed account page, not just the dashboard total. You should see a breakdown for each individual loan listing the current interest rate, balance, and type (fixed or variable). If anything is unclear, call and ask them to walk you through every line on the statement.

- Question 2Is a 17% student loan interest rate legal?

- Answer 2In many cases, yes—especially with private loans, which don’t follow the same rules as federal loans. The rate depends on the contract you signed, your credit at the time, and whether the loan is variable. That said, you can often refinance or negotiate better terms, especially as your income and credit improve.

- Question 3What’s the first move if I realize my rate is extremely high?

- Answer 3First, stop ignoring the statement. Then do three things: list all your loans by rate, shift any extra payments to the highest-rate one, and start shopping around for refinancing options with banks or credit unions. A free session with a nonprofit credit counselor can also help you map out the safest path.

- Question 4Should I focus on interest rate or balance size?

- Answer 4The rate usually matters more than the size if your goal is to pay less over time. A smaller balance at 15% can cost you more in interest than a larger one at 4%. That’s why many experts suggest targeting the highest-rate loan first, even if its balance looks smaller or less scary.

- Question 5Do I have to check my loans every month?

- Answer 5Ideally, you’d glance at them regularly, but let’s be honest: nobody really does this every single day. A realistic rhythm is to do a deeper check every few months, or any time your payment changes, your income shifts, or you’re thinking about new goals like moving, switching jobs, or going back to school.