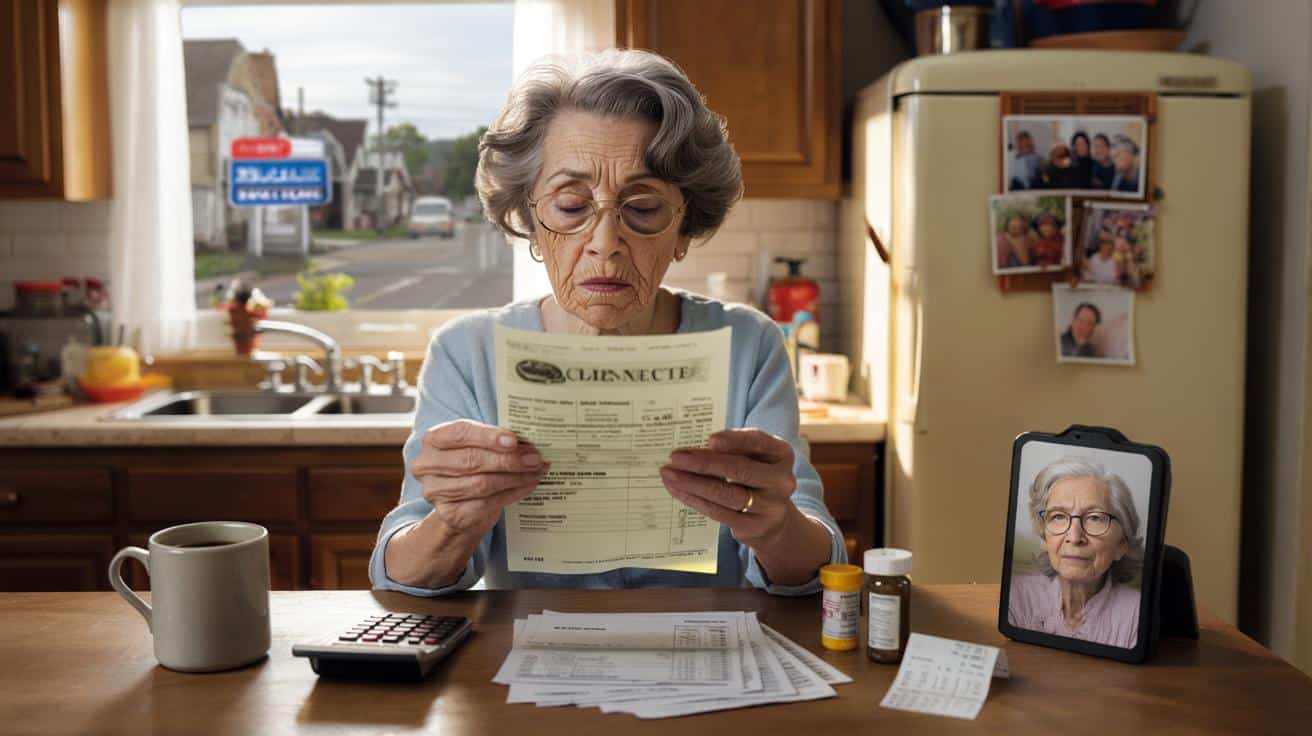

The letter came on a Tuesday, the kind of plain white envelope that usually means a bill or a warning. Mary, 71, sat at her kitchen table, glasses slipping down her nose, coffee going cold as she unfolded the Social Security notice about her 2026 benefits. Her eyes moved straight to the dollar figure. She read it once, twice, then a third time, as if the number might change if she stared hard enough.

Out the window, the price sign at the gas station flickered, climbing again.

That new monthly amount suddenly wasn’t just a number. It meant: groceries or skipped meals, prescriptions or cutting pills in half, birthday gifts for grandkids or a quiet apology.

She grabbed her phone and called her sister.

“Did yours go up too?” she asked.

There was a pause.

“Yeah,” her sister said. “But is it really enough?”

What the 2026 Social Security boost actually looks like

Social Security’s 2026 payment boost is now on the books, and the first reaction most people have is simple: “What does this mean for my check?” The government calls it a cost-of-living adjustment, or COLA, tied to inflation numbers that feel painfully real every time you stand at a supermarket checkout.

The new rates bring a few extra dollars each month for retirees, spouses, survivors, and disabled workers. On paper, it looks like relief. In real life, it feels more like a race where prices are always a few steps ahead.

You’re not imagining that tension. It’s built into how the program works.

➡️ I’m a veterinarian: the simple trick to teach your dog to stop barking without yelling or punishment

➡️ Japan unveils a new toilet-paper innovation “and shoppers can’t believe it didn’t exist sooner”

Picture a retired couple, James and Linda, both in their late 60s, living on Social Security and a small pension in Ohio. In 2025, James was getting about $1,950 a month as a retired worker, while Linda, receiving a spousal benefit, was at roughly $950.

For 2026, their notice shows a few percentage points more. James edges closer to $2,000, Linda’s check climbs toward four figures. On paper, their household is up maybe $70–$90 a month total. That’s a couple of grocery bags. A water bill. Part of a prescription.

They feel a tiny surge of relief, then they walk into the pharmacy and see the new price on Linda’s insulin. The boost suddenly shrinks.

The Social Security Administration adjusts benefits each year based on the CPI-W, a measure of inflation focused on workers’ costs. When that index rises, Social Security tries to keep pace by raising checks the following January. In 2026, the new monthly amounts reflect the inflation pressures of the previous year, not the prices you’re seeing this second.

So retirees, spouses, survivors, and disabled beneficiaries are all playing catch-up with last year’s economy. The base formula stays the same: your work history and earnings decide your “primary insurance amount,” then COLA applies on top. That’s why two neighbors can get wildly different checks, even with the same percentage boost.

The blunt truth is: Social Security is designed as a safety floor, not a luxury ceiling.

New 2026 amounts by category: what your check might feel like

One practical way to think about the 2026 boost is to break it down by who you are on Social Security’s paperwork. Retiree. Spouse. Survivor. Disabled worker. Each label comes with its own starting formula, then the COLA gets applied across the board.

Retired workers see their monthly amount rise first, since they’re the core of the program. Spouses who never earned much on their own wages are tied to that retired worker’s record, usually up to 50% of their full benefit amount. Survivors get a percentage of a deceased worker’s check, and disabled beneficiaries are based on what they would have received at full retirement age.

One small percentage change in COLA ripples through all those categories, like a tide lifting similar but not identical boats.

Take Carla, 59, who became widowed unexpectedly three years ago. She switched from a lower disability benefit to a survivors benefit on her late husband’s record. Each year, she waits for the COLA announcement like other people wait for weather alerts.

Her 2025 survivor benefit brought in about $1,600 a month. With the confirmed 2026 boost, she sees her check inch upward – another few dozen dollars. It helps her cover the heating bill during a cold snap in January, but it doesn’t erase the math she does before every grocery run.

We’ve all been there, that moment when you stand in front of your pantry, mentally tallying what’s left until the next deposit hits your account.

What makes this adjustment confusing is that it’s both automatic and deeply personal. The percentage increase is the same for everyone, yet the lived effect depends on your rent, meds, debt, even your adult kids’ needs. The COLA doesn’t ask whether you’re helping a grandson with college applications or paying your daughter’s phone bill after a layoff.

This is why the 2026 boost can feel like a win and a letdown at the same time. You might see headlines about “bigger Social Security checks,” then open your own letter and feel underwhelmed. That’s not a failure on your part to budget correctly.

It’s a gap between national averages and kitchen-table realities.

How to actually use the 2026 increase so it helps, not vanishes

There’s a quiet trick that the calmest retirees seem to share: they decide what the raise is for before it hits the bank. When you know the dollar amount of your 2026 boost, write that number on a sticky note. Say your increase is $48 a month. That’s not “extra money,” it’s “pharmacy copay” or “food budget” or “emergency fund.”

Assigning that label early keeps the raise from disappearing into random spending. You can even open a separate savings sub-account, rename it “2026 COLA,” and send just the increase there each month.

*It’s amazing how different that small bump feels when it lands where you chose, not where the day pushed you.*

Many people react to a Social Security increase by quietly raising their everyday spending: a slightly nicer grocery cart, a few more takeout meals, an extra streaming service. There’s no shame in wanting small comforts after decades of work. That said, this “lifestyle creep” is exactly how a hard‑won COLA gets swallowed without a trace.

A gentler approach is to split the difference. Maybe 60–70% of the 2026 boost goes to a non-negotiable bill or savings, and the rest is your guilt-free money for coffee with friends, a grandchild’s gift, or that monthly haircut you kept postponing. Let’s be honest: nobody really does this every single day.

But doing it once, clearly, for your 2026 raise can shift your whole year.

“Every January, I sit down with my Social Security letter, a notebook, and a cup of tea,” says Darlene, 73, from Arizona. “I circle the new amount, subtract last year’s, and write that difference at the top of the page. Then I decide: this year, my raise belongs to something that matters. One year it was dental work, last year it was my emergency fund. If I don’t give it a job, it just…evaporates.”

- Compare your 2025 and 2026 notices side by side and highlight the monthly difference.

- Pick one priority: debt, medical, food, savings, or small joy – and “assign” the raise to it.

- Set an automatic transfer for the exact increase amount on the day your benefit hits.

- Tell one trusted person your plan, so they can encourage you when money feels tight.

- Revisit the plan mid-year to adjust if rent, meds, or family needs have changed.

Looking at 2026… and beyond the numbers on the page

The 2026 Social Security boost isn’t just about percentages or charts; it’s about the quiet negotiations you have with yourself each month. You weigh pride against asking for help. Necessity against small pleasures. Fear of running out against the urge to live while you can still get around.

The new monthly figures for retirees, spouses, survivors, and disabled beneficiaries will show up as a line on a government letter. What they turn into – stability, anxiety, or a mix of both – will depend on how you react in the next few weeks.

There’s a conversation here that reaches beyond any one year’s COLA. It’s about how a country treats those who already did their time on the job, those who got sick before they were ready, those who lost a partner too soon. If you feel like sharing that story, even just with a friend over coffee or online in a support group, you’re not just talking about money.

You’re quietly shaping what the next Social Security letter might mean for the people who come after you.

| Key point | Detail | Value for the reader |

|---|---|---|

| Understand the 2026 boost | COLA raises all categories (retirees, spouses, survivors, disabled) based on last year’s inflation | Helps set realistic expectations about how much your check is likely to rise |

| Know your category | Benefit formulas differ if you’re a retired worker, on a spousal benefit, survivor benefit, or disability | Explains why your increase may look different from friends’ and neighbors’ |

| Give your raise a job | Pre-assign the monthly increase to one priority: bills, meds, savings, or small joys | Makes the 2026 bump visible in your daily life instead of disappearing in routine spending |

FAQ:

- Will every Social Security beneficiary get a 2026 increase?Yes. Once the COLA is set, it applies across the board to retirement, spousal, survivor, and disability benefits. The exact dollar amount varies based on your current benefit.

- Does the 2026 boost change my Medicare premium too?COLA and Medicare premiums are separate, but they collide in reality. If Medicare Part B premiums go up, they can eat part of your raise, especially for those with smaller checks.

- Will my 2026 increase push me into paying tax on my Social Security?It might. If your combined income crosses certain thresholds, a portion of your benefits can be taxable, so checking with a tax preparer or free senior tax clinic is wise.

- Do spouses and survivors get the same percentage raise as retired workers?Yes, the COLA percentage is the same. The difference is that their base benefit is a percentage of the worker’s amount, so the final dollar increase can feel smaller.

- Can I ask Social Security to recalculate my benefit if I still work in 2026?If you keep working and earn more than some past years, SSA periodically recalculates your benefit using your highest 35 earning years. That’s separate from COLA and can boost future payments.